Why IUL Is a Bad Investment: The Ugly Truth Most Agents Won’t Tell You in 2026

Introduction

“A magnifying glass over a life insurance policy document with a red warning stamp, symbolizing hidden risks in IUL investments. Clean, minimal background.”

You just sat through a 90-minute insurance presentation. The agent showed you colorful charts, mentioned the S&P 500, promised tax-free growth, and made it sound like indexed universal life insurance (IUL) is the best financial product you have never heard of. Now you are wondering: is this actually a good idea?

Here is the short answer: why IUL is a bad investment is a question more people should be asking before they hand over their money. This article gives you the full picture. No sales pitch. No jargon fog. Just the real mechanics, the real costs, and the real alternatives you should consider instead.

By the end, you will understand exactly what IUL is, how it actually works, where it goes wrong for most people, and what financial experts recommend instead.

What Is an Indexed Universal Life (IUL) Policy?

Indexed universal life insurance is a type of permanent life insurance. It blends a death benefit with a cash value component. The cash value is tied to the performance of a stock market index, like the S&P 500, but you are not actually investing in that index. That distinction matters enormously.

Here is how the basic structure works:

- You pay a monthly premium, which is usually much higher than a term life policy.

- Part of that premium covers the cost of insurance (COI).

- The rest goes into the cash value account.

- The insurance company credits your account based on index performance, subject to a cap and a floor.

The floor sounds great, zero percent in a down year. But the cap, often 8 to 10 percent, limits how much you actually earn in a strong year. When the S&P 500 returned 26.9% in 2023, most IUL holders saw a fraction of that gain.

The 6 Real Reasons Why IUL Is a Bad Investment

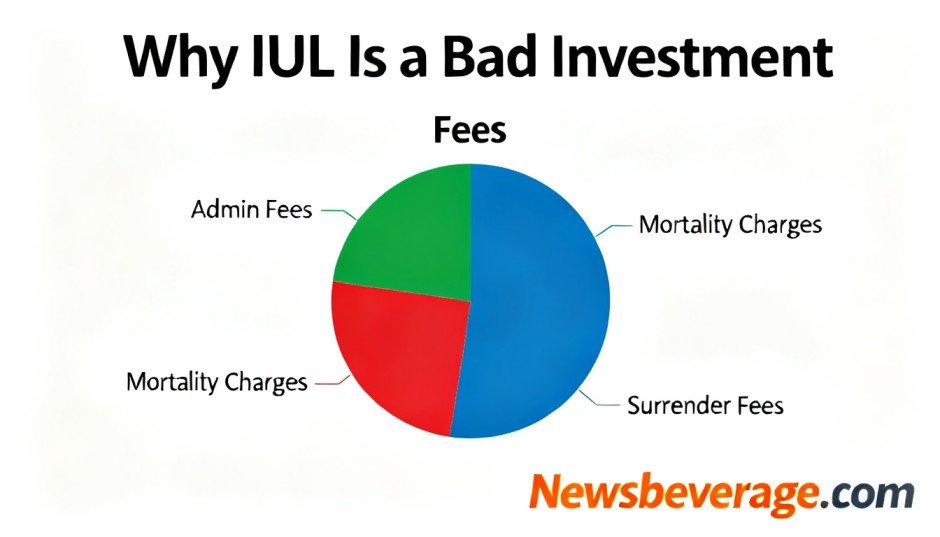

1. The Fees Are Staggering and Well Hidden

This is the biggest problem. IUL policies carry multiple layers of fees that eat into your returns before they even post to your account. Most agents skim over these or bury them in a 60-page illustration document.

Here are the fees you typically face:

- Premium load: 5 to 10 percent taken right off the top of each payment.

- Cost of insurance (COI): This increases every year as you age. In your 60s, it can become enormous.

- Administrative fees: Monthly charges just for having the policy.

- Surrender charges: If you leave in the first 10 to 15 years, you pay heavy penalties.

- Spread or participation rate adjustments: The insurer can lower your participation rate at any time.

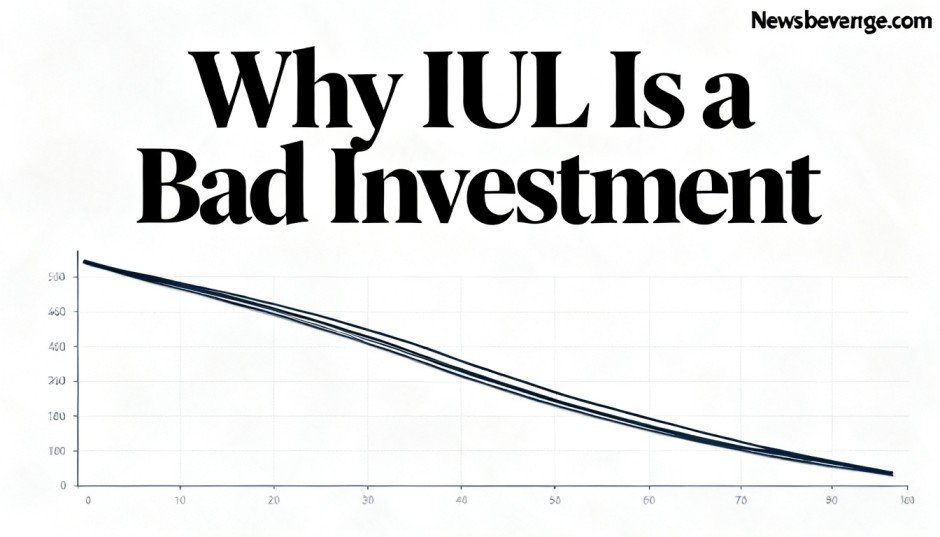

Studies from Consumer Federation of America have found that the internal rate of return on many IUL policies after fees is 1 to 3 percent over 20 years. A simple index fund, on the other hand, historically returns around 7 to 10 percent annually over the same period.

1–3%

Avg. IUL after-fee return (20 yrs)

7–10%

Historical S&P 500 index fund return

15 yrs

Typical surrender period

2. Caps Kill Your Growth in Bull Markets

Insurance companies love to advertise that your money participates in market upside. What they say less loudly is that your upside is capped. In practice, a 10 percent cap means that if the index returns 25 percent, you get 10 percent, minus any spread or participation rate reduction.

Over a long time horizon, missing those strong years has a dramatic compounding effect. A dollar growing at 7 percent for 30 years becomes about $7.61. A dollar growing at 3 percent for 30 years becomes about $2.43. That gap is your retirement.

3. Insurance Costs Rise as You Age

The cost of insurance is not fixed. It rises every single year because your risk of dying increases. In your 30s and 40s, this cost is manageable. In your 50s and 60s, the cost of insurance can start consuming most of your premium and begin eating into your cash value.

This creates what is called a policy lapse risk. If your cash value shrinks below what is needed to cover the COI, your policy lapses. You lose your death benefit and potentially face a surprise tax bill on gains you thought were tax-free.

Policy lapse is one of the most devastating outcomes in personal finance. You pay premiums for 20 years, the policy collapses in retirement, and the IRS treats your accumulated gains as ordinary income in the year the policy lapses.

4. The Illustrations Are Almost Always Misleading

Agents are required to show you a policy illustration, which is a projected growth table over time. The problem is that these illustrations use best-case or optimistic interest crediting scenarios that almost never match reality.

A 2015 report by the Society of Actuaries found that illustrated returns for IUL products frequently exceeded what policyholders actually received, sometimes by 2 to 4 percentage points annually. The National Association of Insurance Commissioners (NAIC) has repeatedly tried to tighten illustration rules because of this problem.

If your illustration assumes 7 percent credited interest but you actually receive 3 to 4 percent due to caps and participation rate adjustments, the entire financial model falls apart.

5. It Is Not Actually “Tax-Free” in Many Situations

Tax advantages are the biggest selling point of IUL. The idea is that your money grows tax-deferred, and you access it through policy loans that are not taxable income. This is technically true but comes with serious asterisks.

- Policy loans accrue interest. If you borrow too aggressively, the loan balance can grow until it exceeds your cash value, causing a lapse.

- If the policy lapses with an outstanding loan, the entire loan amount becomes taxable income in that year.

- Withdrawals above your basis are taxable as ordinary income, not capital gains.

- The tax advantage disappears if the policy fails the IRS’s Modified Endowment Contract (MEC) rules, which can happen if you overfund too quickly.

The “tax-free retirement income” strategy only works perfectly if the policy stays in force for life, you manage loans carefully, and the insurance company does not reduce your cap or participation rate. That is a lot of ifs.

6. You Lose Investment Control and Flexibility

When you put money into a 401(k) or a Roth IRA, you choose your investments. You can shift allocations, switch funds, or move to cash. With an IUL policy, the insurance company holds your money and decides the terms of your participation rate, your cap, and your floor. They can change these terms at almost any time.

If market conditions change and the insurer finds the current caps unprofitable, they can lower your cap. You are not investing in the market. You are entering a contract with an insurance company, and they hold most of the cards.

Who Actually Benefits from IUL?

To be fair, IUL is not a scam. In narrow circumstances, it has legitimate uses. You might benefit from IUL if all of the following apply to you:

- You have already maxed out your 401(k), Roth IRA, and other tax-advantaged accounts.

- You have a high income and need additional tax deferral strategies.

- You have a genuine long-term insurance need (30 or more years).

- You fully understand all the fees, risks, and moving parts.

- You work with a fee-only advisor, not a commission-based agent.

For the vast majority of working Americans, none of these boxes are checked. Most people are sold IUL before they have even contributed the maximum to their employer’s retirement plan.

What Should You Do Instead?

The good news is that the alternatives are simpler, cheaper, and historically more effective.

| Option | Best For | Tax Advantage | Avg. Return |

|---|---|---|---|

| Roth IRA | Long-term retirement savings | Tax-free growth and withdrawals | 7–10% (index fund) |

| 401(k) / 403(b) | Employer match, tax deferral | Tax-deferred growth | 7–10% (index fund) |

| Term Life + Invest the Rest | Pure insurance need | None, but low cost | 7–10% (separate investment) |

| HSA | Healthcare + retirement | Triple tax advantage | Varies |

| IUL | High-income, fully funded savers | Tax-deferred with caveats | 1–4% net of fees |

The “Buy Term and Invest the Difference” Strategy

Financial planners like Dave Ramsey and Suze Orman have long advocated for this approach. Buy a term life insurance policy for pure death benefit protection. It costs a fraction of a permanent policy premium. Then take the money you saved and invest it in low-cost index funds through a tax-advantaged account.

Over 30 years, this approach consistently outperforms IUL in real-world scenarios. You get better returns, more flexibility, lower risk, and full control over your money.

What the Research and Experts Say

This is not just a matter of opinion. Here is what the research shows:

- A 2022 white paper from the National Bureau of Economic Research found that complex life insurance products with investment components underperform simpler alternatives for most households.

- Fee-only financial advisors surveyed by NAPFA consistently rank IUL as a poor primary investment vehicle.

- The SEC and FINRA have both issued investor alerts warning consumers to carefully scrutinize illustrations and fee disclosures in insurance-based investment products.

- Clark Howard, a consumer finance expert with a national radio show, has labeled IUL as one of the most oversold financial products in America.

Red Flags to Watch for in an IUL Sales Pitch

If you are sitting in front of an agent, watch for these warning signs:

- They show you an illustration with a high assumed interest rate (above 6 percent).

- They do not clearly explain all the fees in plain dollar amounts.

- They focus heavily on the “tax-free retirement income” angle before asking about your existing accounts.

- They pressure you to decide quickly or suggest this is a limited-time product.

- They earn a commission on the sale (most IUL agents earn 50 to 100 percent of your first-year premium).

- They do not mention the cost of insurance or how it changes over time.

Always ask an agent: “Can you show me the guaranteed column of this illustration, not the projected column?” The guaranteed column reflects the worst-case scenario the insurer is actually contractually bound by. It is usually sobering.

Also read Newsbeverage.com

Email: johanharwen314@gmail.com

Author Name: Johan Harwen